Book a Free Consultation

We have to reflect on the U.S. employment data that was released on Friday, February 2nd 2018.

Non-Farm Payrolls were stronger than expected at +200K, though taking account of revisions (Dec 160K vs. prov. 148K, Nov 216K vs. 252K), this was generally in line with forecasts.

The 3-month average moved up to 192K which is double the Fed’s assumption on the breakeven pace of monthly payrolls growth.

Services unsurprisingly led the way with a gain of +139K, in no small part by a +15K recovery in retail jobs following the 26K drop in December, and continued strength in leisure/hospitality (+35K), sectors which obviously tend to have a high preponderance of low paid jobs.

Manufacturing still posted a 15K gain, off the 25-30K rate that has been booked in recent months, but it is most definitely a good figure.

The Unemployment Rate was unchanged 4.1% although do note there was a small uptick in the Underemployment Rate to 8.2% from 8.1%, and no change in the Participation Rate at a still rather soft 62.7%.

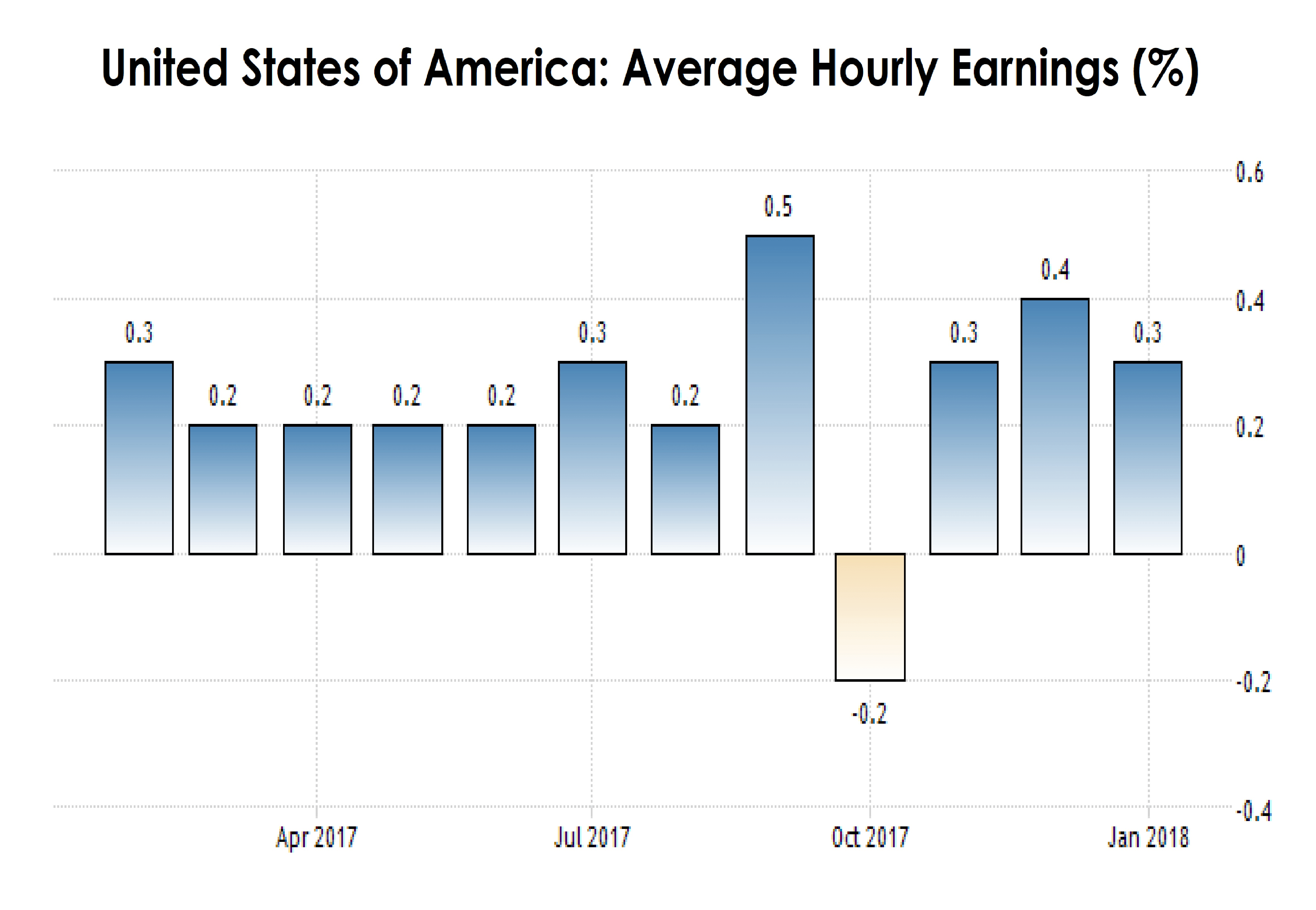

What spooked the markets was the surge in Average Hourly Earnings that not only beat expectations at 0.3% MoM cf. a forecast of 0.2% MoM, but also saw December revised up to 0.4% MoM from 0.3%. These combined to lift the YoY rate up to a nine year high of 2.9%.

That was enough to unsettle equities and curiously the U.S. Treasury market saw yields to 2-Years decline and from 3-Years and out rise. This was an acknowledgment that the hawks in the FOMC will see this as reason to raise Fed Funds three times this year.

Worries about the impact of a tightening job market on the prospects for inflation and a surge in bond yields sent equities spiraling lower on Friday.

Dow Jones Industrials -665.75 -2.54%

S&P 500 – 59.85 -2.12%

Nasdaq -144.92 -1.96%

For the Dow this was its biggest daily percentage loss in 20 months and the biggest daily point fall in the Dow since December 2008 during the financial crisis.

On Friday Wall Street’s three major indexes logged their biggest weekly losses in two years, after closing at record highs the previous week. The S&P 500 and Dow saw their worst weeks since early January 2016 while Nasdaq had its worst week since early February 2016.

At the close in Frankfurt, the DAX lost 1.68% to hit a new 3-months low, while the MDAX index declined 2.05%, and the TecDAX index lost 1.51%.

French stocks were lower after the close on Friday, as losses in the Basic Materials, Consumer Services and Industrials dragged the CAC 40 lower by 1.64%, while the SBF 120 index fell 1.60%.

The FTSE 100 lost 0.63% to reach 7,443.43 points, its lowest close since December 14 to round out a horrid week in which it lost more than 200 points. UK-listed miners led the daily declines, with Evraz suffering the biggest fall, closely followed by Glencore.

The U.S. Dollar in its best week so far in 2018, even though the Swiss Franc and Euro extended their weekly advances for a seventh and fourth week, respectively.

The jump in U.S. Dollar denominated bond yields and retreat in equities point to a larger portfolio adjustment and not simply a short-covering bounce in the Dollar. Naturally, price action in the days ahead is key to this opinion.

The Dollar Index rose for the first week since the weekend ending December 15 arresting the recent sharp downside momentum.

Initial resistance is seen near 89.65. A convincing break gives it potential toward 90.85-91.00.

The Euro continues to be resilient. It did not fall to new lows for the week after the US jobs data and held above EURUSD1.24. Nevertheless, the upside momentum has stalled, and interest rate differential is such that it costs to belong the Euro if it is going to simply rend sideways, if not lower.

Important support is not at EURUSD1.24 as last week’s lows but EURUSD1.2335, and a break of it targets EURUSD1.2300. That would infer a correction rather than consolidation.

The U.S. Dollar rose 1.45% against the Japanese Yen last week; its best performance in around 5 months. USDJPY finished above JPY110.00 but stalled near the 20-day moving average in front of JPY110.50

Sterling posted a 0.3% decline last week so breaking a six-week, 7.8% rally. Disappointing UK economic data, more internal woes for the governing Conservatives and a harder line from the EU provided the incentives for the mild profit-taking.

That said, GBPUSD finished above the week’s lows near 1.3980 but appears headed for a test to the GBPUSD1.3800-$1.3900 area.

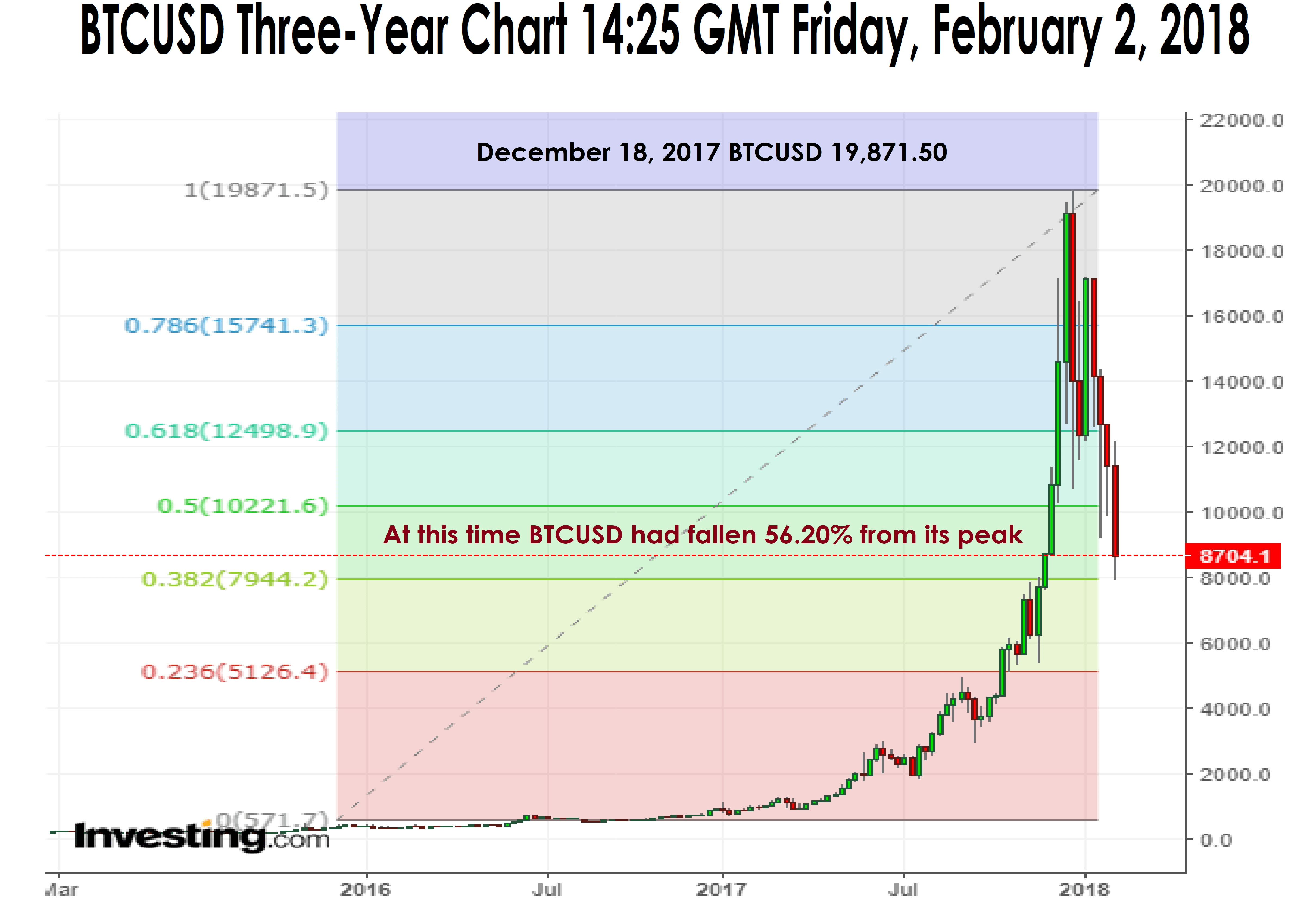

Bitcoin slumped to a new YTD low as negative news from India and Netherlands put pressure on it. The cryptocurrency recorded its worst monthly performance in January.

Bitcoin fell to its lowest level this year on February 2, touching BTCUSD 7974.14 at 12:00 GMT. This was the lowest point since November 24, 2017, when it was in the middle of an impressive rally that surprised investors.

In January, Bitcoin had the worst performance since the same month of 2015, falling by about 30%. The cryptocurrency is going through a rough patch amid a series of unfavorable fundamentals as outright bans, restrictions and tax levies are being rapidly applied.

The Netherlands is showing signs that it may ban Bitcoin trading. Finance minister Wopke Hoekstra said that parties in the House of Representatives want to limit crypto market activity, perhaps even to the point of banning it. It seems we will get the final verdict in a few weeks.

Gold prices fell sharply amid Dollar strength. Gold futures for February delivery on the Comex division of the New York Mercantile Exchange rose by USD9.80, or 0.73%, to USD1,337.80/ Troy Oz.

In other precious metal trade, silver futures fell 2.48% to USD16.73/Troy Oz while platinum futures fell 0.85% to USD999.20/ Troy Oz. Copper fell 0.65% to USD3.19/lb.

Oil prices finished lower on Friday to tally a loss for the week, as traders weighed a steady increase in U.S. output against OPEC’s ongoing efforts to drain the market of excess supplies.

U.S. West Texas Intermediate (WTI) crude futures for March delivery fell 35 cents, or around 0.5%, to close at USD65.45/barrel.

Janet Yellen chaired her final meeting as boss of the US Federal Reserve, America’s powerful central bank, on Wednesday last week. She will formally hand over the job to Jerome Powell on Monday, February 5th

Yellen took over from Ben Bernanke in 2014, becoming the first female Fed chair. She is a respected academic economist, and on her watch the U.S. has performed extremely well with GDP growth picking up and unemployment falling to its lowest levels since the Bill Clinton boom of the late 2000s.

She took the decision to activate the first interest rate hike in a decade, when the Fed raised its lending rate from 0.25-0.5% in December 2015.

The markets had been careful primed to expect the monetary tightening and the financial sell-offs that many had feared did not materialise.

On her watch the Fed has gone on to raise rates a further four times, with the most recent coming in June 2017. A fifth is expected in March and the central bank is also gradually selling down its $4.5 trillion worth of assets, accumulated in the years of quantitative easing after the global financial crisis to help support the US economy.

In general economist’s credit her with being an extremely competent and level-headed Fed chair.

So, one wonders why is she just serving one term? That is because President Trump (republican) chose not to reappoint her, even though most Fed chairs in recent history have served two terms. Yellen is a Democrat, but previous presidents have happily reappointed chairs associated with the opposite party.

Trump opted for 64-year-old Jerome Powell, a veteran private equity financier, registered Republican, and a member of the Fed board since 2011.

Powell is regarded as a centrist on monetary tightening, meaning that he is seen as less likely to jack up rates rapidly. Yet some are still worried about the possibility that Mr Powell might contribute to a dangerous deregulatory crusade being led by the White House and supported by Republican congressmen who are heavily funded by Wall Street banks.

Powell’s biggest challenge will be protecting the independence of the Fed from likely political pressure from the Trump White House in the years ahead.

Furthermore, with many analysts worried that the US stock market is in the grip of a speculative bubble, and with recent Republican tax cuts set to stoke the US economy still further, Powell’s crisis-handling skills may also be tested sooner rather than later.

Monday 5th

09:30 UK Services PMI January expect 54.3 previous 54.2

15:00 USA ISM Non-Manufacturing PMI January expect 56.5 previous 56.0

Tuesday 6th

15:00 USA JOLTs Jobs Openings December expect 6.038m previous 5.879m

Wednesday 7th

15:00 USA Crude Oil Inventories previous 6.776m

Thursday 8th

12:00 UK BoE Inflation Letter and Report

BoE MPC Rate Decision expect 0.50% previous 0.50%

Friday 9th

O9:30 UK Manufacturing Production MoM December

expect 0.3% previous 0.4%

Have a great week.